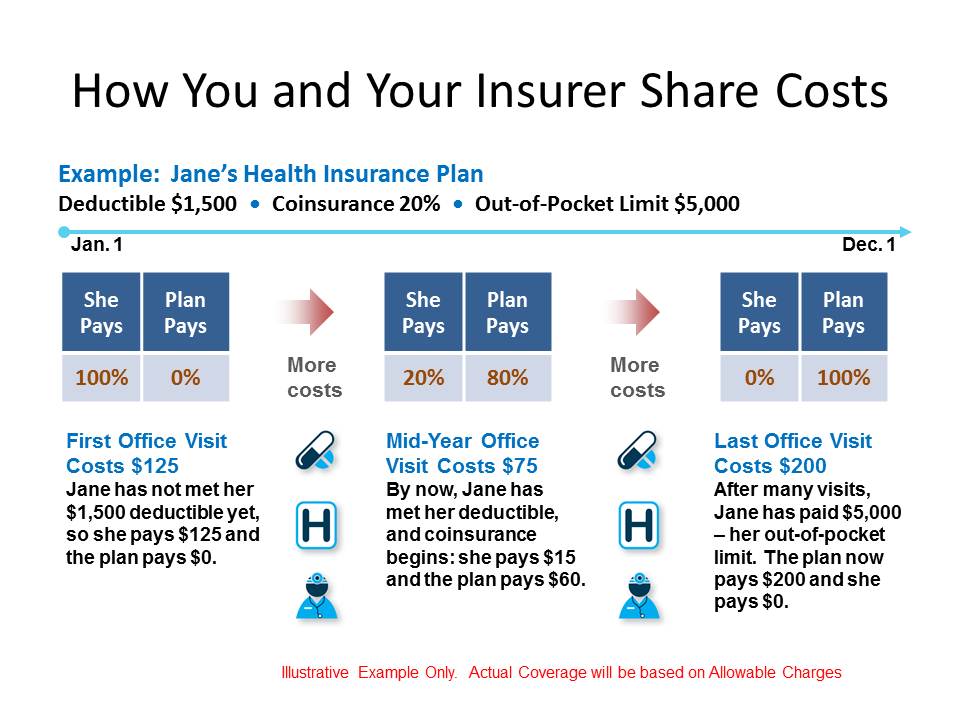

You've researched rates and the health strategy you've chosen costs $175 per month, which is your premium. In order to keep your benefits active and the plan in force, you'll need to pay your premium on time each month. Deductible A deductible is a set quantity you have to pay every year toward your medical expenses before your insurer begins paying.

Your strategy has a $1,000 deductible. That indicates you pay your own medical costs up to $1,000 for the year. Then, your insurance coverage kicks in. At the beginning of each year, you'll need to satisfy the deductible once again. Coinsurance Coinsurance is the portion of your medical expense you show your insurer after you've paid your deductible.

You have an "80/20" strategy. That means your insurance provider spends for 80 percent of your costs after you have actually satisfied your deductible. You spend for 20 percent. Coinsurance is various and separate from any copayment. Copayment (or "copay") Your copayment, or copay, is the flat fee you pay whenever you go to the doctor or fill a prescription.

Copays do not count towards your deductible. Let's say your strategy has a $20 copayment for routine medical professional's check outs. That suggests you need to pay $20 each time you go. Copayments are different than coinsurance. Like any kind of insurance coverage plan, there are some costs that may be partly covered, or not at all.

Less apparent expenses might consist of services offered by a physician or medical facility that is not part of your strategy's network, plan limitations for particular sort of care, such as a specific number of check outs for physical therapy per benefit duration, in addition http://simonnpcc943.fotosdefrases.com/get-this-report-about-how-to-file-an-insurance-claim to non-prescription drugs. To help you discover the ideal plan that fits your spending plan, appearance at both the obvious and less obvious costs you may anticipate to pay.

If you have different levels to pick from, choose the greatest deductible quantity that you can conveniently pay in a fiscal year. Discover more about deductibles and how they impact your premium.. Quote your overall variety of in-network physician's check outs you'll have in a year. Based upon a plan's copayment, add up your total cost.

Even plans with comprehensive drug coverage might have a copayment. Figure in dental, vision and any other regular and required care for you and your family. timeshare resale scams If these expenditures are high, you may want to think about a plan that covers these costs. It's a little work, however taking a look at all costs, not simply the apparent ones, will assist you discover the strategy you can afford.

The Greatest Guide To How To Get Free Birth Control Without Insurance

Attempting to determine your annual healthcare expenses? There are several pieces of the expense puzzle you need to consider, including your premiums, deductible, coinsurance and copay. Below is an explanation of each and examples that demonstrate how people utilize them to spend for healthcare - how much is flood insurance in florida. For information on your plan's out-of-pocket costs and the services covered, check the Summary of Benefits and Coverage, which is included in your enrollment products.

Higher premiums usually suggest lower deductibles. An example of how it works: Trisha, 57, plans on dedicating herself to her 3 grandchildren after she retires. Understanding she'll require to maintain her energy, she just signed up for a different health care plan at work. The strategy premium, or cost of coverage, will be taken out of her incomes.

That is necessary given that Trisha assured her grown kids she 'd be more persistent about her own health. Find out more about how health plans with greater premiums typically have lower deductibles. Her new plan will keep out-of-pocket expenses predictable and workable due to the fact that as a former cigarette smoker with breathing issues, she requires to see physicians and experts routinely - how to fight insurance company totaled car.

In the meantime, she's conserving cash, listening to her doctors and enjoying time with her family on weekends. What is a deductible? A deductible is the amount you pay out-of-pocket for covered services prior to your health insurance starts. An example of how it works: Courtney, 43, is a single lawyer who just bought her first home, a condominium in Midtown Atlanta.

When she felt a swelling in her breast throughout a self-exam, she instantly had it took a look at. Thankfully, doctors told her it was benign, but she'll require to go through a lumpectomy to have it gotten rid of. Courtney will pay of pocket for the treatment up until she meets her $1,500 deductible, the quantity she pays for covered services before her health insurance contributes.

In case she has more medical costs this year, it's good to understand she'll max out the deductible immediately so she won't need to pay complete cost. Discover how you can save money with a health savings account. What is coinsurance? Coinsurance is the percentage of the costs you pay after you satisfy your deductible.

Their 3-year-old just recently fell at the playground and broke his arm. The family maxed out their deductible currently, so Ben will be responsible for only a portion of the costs or the coinsurance billed for the procedure to reset and cast the break. With his 20 percent coinsurance, he'll end up paying a couple of hundred dollars for the health center visit.

Unknown Facts About What Is A Whole Life Insurance Policy

Learn how healthcare facility strategies can help you cover costs prior to you fulfill your medical deductible. What is copay? Copays are flat charges for certain sees. An example of how it works: Leon, 34, is a married forklift operator from Jacksonville, FL. He's an avid runner, but recently has actually had irritating knee discomfort and swelling.

Thankfully, his health plan has some set expenses and just requires $30 copays for check outs to his regular physician and $50 copays to see specialists like an orthopedist. (He also when paid a $150 copay the night he landed in the emergency clinic when his knee was so inflamed he couldn't bend it.) Having these set charges provides Leon assurance considering that he and Leah are conserving to buy a kayak.

His copays encompass physical treatment gos to, where he'll pay $20 for each session. Leon's figured out to get whatever back on track so he and Leah can go back to doing the important things they love: hanging out together outdoors. By discovering how premiums, deductibles, coinsurance and copays work, you can better understand your health care costs.

Some health insurance policies need the insured individual to pay coinsurance. Coinsurance means that you will share some portion of the payment for your healthcare expenses with your health insurance provider. Hero Images/ Getty Images When marriott timeshare resale you are selecting your medical insurance policy, you might have several options, including a few plans with the option of coinsurance.