Not having medical insurance is a threat, not only for the preservation of your health, however also your financial security. 1. You buy car insurance because it assists you pay for repairs if it breaks down or you have an accident. Health insurance is a.

little.

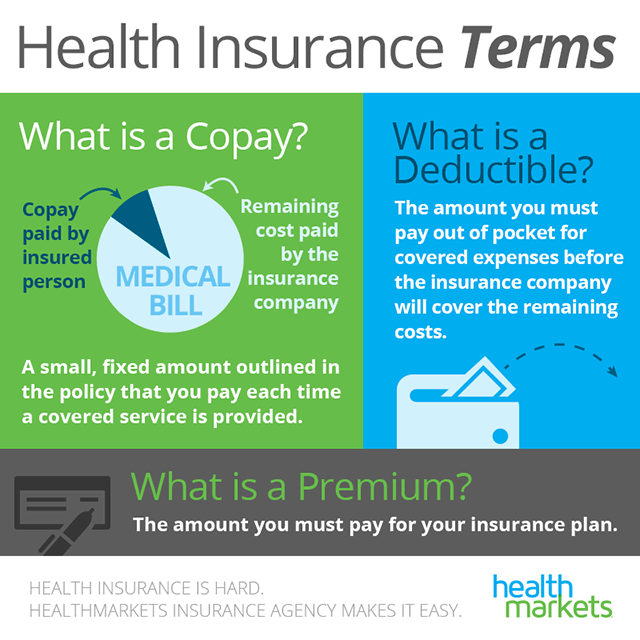

like that. Health insurance assists you pay for medical professionals, medical facilities, medications and more if you get sick or have a mishap. What's more, health insurance assists you spend for preventive care, like yearly vaccinations, inspect ups and wellness programs, so you're less likely to become ill. You and your medical insurance business become" partners" who interact to spend for your healthcare. This is called. Your payment is called an In some cases, your employer pays part of the month-to-month and you pay part. Health insurance with a Copay+ Deductible +Coinsurance 2. Health Plans with a Deductible+ Coinsurance( No Copay), Typically, copays are for doctor's office, urgent care and emergency room sees, and prescription drugs. However read your health insurance information to be sure.( Copays don't count towards paying your deductible.) You'll spend for any services or materials not covered by a copay, when you examine out, until you've satisfied your deductible for the strategy year. After you satisfy your deductible, then you pay part of the costs (state 20%) and your insurance pays part of the expense (state 80% )until you've paid your coinsurance for the plan year. Individuals usually buy a strategy with copays so they have a better idea of the expense of each visit before they go. Plans with copays can be more pricey, however are a good choice if you know you'll require to visit the physician a lot. You'll pay for any services or products, when.

you have a look at, up until you have actually satisfied your deductible for the plan year. After you satisfy your deductible, then you pay part of the expense( state 20%) and your insurance pays part of the expense (state 80 %) till you have actually http://stephenydxn891.cavandoragh.org/the-greatest-guide-to-how-much-insurance-do-i-need paid your coinsurance for the strategy year. (Together, this is the most you'll pay throughout the strategy year.) till the plan year ends or you change insurance coverage strategies. This is an excellent choice if you're reasonably healthy and don't need to check out the physician a lot. Physicians don't typically get the complete cost of their services. Your insurance coverage negotiates a lower rate for you from your doctor. What does homeowners insurance cover. The doctor joins your insurance provider.

's of health care service providers and accepts charge less so you pay less. This is called being If you pick a physician who is, and not a partner with your insurer, you may need to pay part or all of the bill yourself. Your insurance and the medical professional have actually consented to a set cost for the health services you get - How much is gap insurance. This is a chart that shows the amount: your physician billed you your insurance enables the medical professional to bill you your insurance coverage paid the physician you conserved you owe if you haven't paid your deductible or coinsurance How to Read Your EOB All health plans are not the exact same! Your plan may be extremely various from what we're showing here. Prior to you buy a plan, make certain to check out all the details about your expense sharing responsibilities and talk with an insurance coverage expert to read more. In the past, the majority of people had company health insurance. Their business did all of the research study, picked the insurance provider and selected plan choices for workers. This is also called group protection or group insurance. But, a lot has altered over the last few years. Challenging economic times have required numerous companies to cut costs. Increasing health care costs have actually made it tough for companies to spend for health insurance. New and more expensive technologies, treatments and drugs have actually emerged, adding costs. Due to these factors and others, a growing trend is for people to either partially or completely spend for their own health insurance coverage. To help you understand your choices, we'll look at both specific and employer-sponsored strategies, describing and comparing them. Individual Insurance is a health policy that you can purchase for just yourself or for your household. Individual policies are also called personal health plans. If you 'd like, you can deal with an insurance coverage representative to help you go over different plans and costs. You might be qualified for a.

aid from the government to acquire an Affordable Care Act-compliant specific strategy. This can conserve you money on your medical insurance. You may be qualified for a subsidy if your employer does not use cost effective health protection and your home earnings is no more than 400% above the federal poverty line. Benefits of a private strategy: You can choose the insurer, the plan and the alternatives that meet your needs. You can renew or alter health insurance plans, options and medical insurance companies during the yearly Open Enrollment period. Your plan is not tied to your job, so you can alter tasks without losing your coverage. You can pick a strategy that consists of the doctors and medical facilities you trust. You may be eligible for a subsidy from the federal government.

to assist pay for your insurance coverage. Medical Shared offers numerous affordable private health insurance that can satisfy your needs. Employer-sponsored medical insurance is a health policy picked and bought by your company and offered to qualified how do you get out of a timeshare workers and their dependents. Your employer will usually share the cost of your premium with you. Advantages of a company plan: Your company frequently splits the cost of premiums with you. Your company does all of the work picking the strategy options. Premium contributions from your company are exempt to federal taxes, and your contributions can be made pre-tax, which reduces your taxable income. Choosing whether to register in a health insurance coverage plan through your employer or whether to acquire a private, major medical plan on your own can be confusing. There can be considerable distinctions in versatility, benefit alternatives and costs. The following table summarizes some similarities and differences that can assist you determine what will best fit your needs. an employer-sponsored group strategy can differ depending upon several factors. These include your earnings, where you live and whether your company offers a group medical insurance strategy. Below are some averages for annual premium costs for employer and specific plans: Typical Yearly Premium Cost for One Person Individual Plan$ 4,632. 00 1 Individual Plan with Premium Tax Credits$ 1,272. 00 1 Employer-Sponsored Strategy( Employer and worker typically share this expense )$ 6,435. 00 2 While averages can give you a concept of normal expenses, the real story is frequently.

The Ultimate Guide To How Does Whole Life Insurance Work

more complicated. In numerous states, specific plans are cheaper - How does life insurance work. That's due to the fact that private health insurance coverage spreads the risk over a big group possibly Additional reading countless individuals depending upon the plan and insurer.